Morning Comment: A Second Warning Shot Across the Bow

It looks like we missed a very compelling week in the markets last week...as the S&P 500 looked like it was finally going to break out of its seven-week sideways range, but fell back within it by the end of the week. However, it is still quite close to the top-end of that range, so we certainly cannot call it a "failed breakout.".....The weakness in the mega-cap tech stocks that developed as the week progressed...despite some good earnings reports from several of them...was the key catalyst for the pull-back from the highs. Yes, there was more talk about regulation for some of these companies...and we're sure that did have an impact...but that “regulation issue” is not new-news either. Therefore, we strongly believe that the overbought condition that many of these names had reached early last week played a key role in the decline as well. (As we highlighted recently, stocks like AMZN and TSLA had become extremely overbought and thus they had become ripe for a meaningful decline.)

Of course, most pundits will say the decline was only fundamentally based...but they never spent any time working as a trader, so they fully don’t understand what really moves markets. These stocks were ripe for pull-backs...no matter what happened on the fundamental side of things...and the fact that many of them got clobbered despite positive earnings results was a clear indication that this is true.

More importantly, this was the second big decline in successive weeks in these mega-cap names (the FAANGs...plus MSFT, NVDA & TSLA). When the first one took place (on July 13th), we called it a “shot across the bow” for the group (and the stock market). We believe that last week’s action was a second “shot across the bow”...and that investors should take heed. In other words, we believe that investors should now be looking to shift their strategy in these names. Instead of buying them on weakness, they should be taking some profits on any bounces. We are not saying that they should take their holdings down to zero, but “trading around” current positions should provide a great opportunity to buy these names back at much lower levels before the year is over........The third “shot” may not come for another couple of weeks, but when it comes, it could be a “direct hit”...which could/should have an impact on the broad stock market as well.

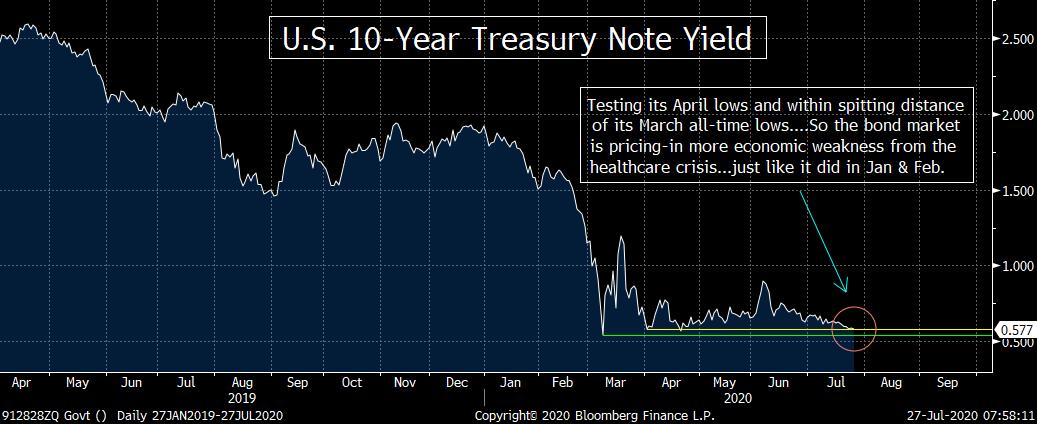

The stock market was obviously not the only market that saw a big move last week. The yield on the 10-year Treasury note fell to a level not seen since April...and is now trading within spitting distance of its March all-time lows. (First chart below.) This is very reminiscent of what we saw in January & February...when the bond market saw (in advance) that the economy was going to see some meaningful weakness from the healthcare crisis before the stock market figured it out.

We also saw a big rally in gold. (When gold broke above the key $1,750 level, we said it would fuel a very quick rally up to its old highs...and that is exactly what happened.) The yellow metal is trading higher again this morning. It's starting to get quite overbought...with a RSI reading of more than 86, therefore it should see at least a "breather" at some point soon...so traders should be a bit wary about aggressively chasing the yellow metal up at these levels right now.

We'd also note that the dollar broke below both of the key support levels we highlighted before we left for vacation...as the DXY dollar index not only closed below 96, but it also fell below 95 last week. (This obviously has had an impact on gold.). It is getting quite oversold...with its daily RSI chart falling towards 20. That is very close to the 19.8 reading we saw at the March lows for the greenback, so we should be getting close to a near-term bounce soon. However, the meaningful move below the key support levels we have been harping on for the dollar is a major red flag for the dollar for the intermediate and long-term. Therefore, unless any short-term bounce turns into a very strong one, investors are going to have to adjust their strategy when it comes to several different asset classes (i.e. commodities and many emerging markets). (Third chart below.)

On the positive side of things, it is quite bullish that the late-week decline in the stock market did not cause the HYG high yield ETF to fall. In fact, the HYG saw a decent advance last week. We also noticed that credit spreads did not widen out. Since these two markets tend to be leading indicators for the stock market, it's a good sign that they are not showing any stress. However, since it is our contention that the Fed is now a lot more concerned about the credit markets than the stock market, the fact that the credit markets remain stable just might mean that the Fed will not respond to a correction in the stock market...by turning the liquidity spigots wide open again (after pulling back on that liquidity significantly since early June).

Don't get us wrong, if the stock market saw another major decline, it would have an impact on the credit markets...so the Fed should still come to the rescue if we see a pick-up of stress in several different markets. However, it seems to us that a lot of pundits think that the Fed would not even let the stock market take a breather...while we believe that they would not care one bit...as long as the credit markets remained stable.

Our real point (the point we've made on several occasions in recent weeks) is that history shows that the Fed does not flood the market with liquidity when the stock market is at/near all-time highs. They only do it after the stock market has been hit hard...and/or there is some stresses developing in the credit markets. Again, they'll want avoid a deep bear market, but a 10%-15% dive is something they could live with...as long as the credit markets acquiesce. Besides, that kind of pull-back will help the markets from forming another massive bubble. This is NOT something most pundits are considering right now. They believe that the Fed will do what ever it takes to keep the stock market rallying. History tells that this might not be the case. In fact, we would argue that it is not the case.

There are a million things we could review from last week...but since most of you were not on vacation (like we were)...it really wouldn't help you much by trying to touch-on all aspects of last weeks moves. Therefore, we will address those issues as if/when they develop further as we move through this week...and into August. However, we do want to reiterate something we focused on before we left for vacation. We continue to believe that the situation with China could prove to be a pivotal one over the next few months. (Needless to say, it should be equally important over the longer term as well.)

We touched-on this issue just over a week ago...and others have done the same since then...so we won't spend too much time regurgitating what we said back then. We'll simply reiterate that China has been taking advantage of the current situation in the U.S....to push VERY hard on several of their long-term initiatives. They're taking advantage of the election year (where the President doesn't want to upset the markets)...and they're taking advantage of our struggles on the Covid-19 healthcare crisis. They have pushed hard on Taiwan...in the China South Sea...and (especially) in Korea...to name just a few. They want to push the line as far as they can now...before another round of significant push-back from the U.S. takes place (which WILL take place...no matter who wins the White House and Congress next year).

However at some point, the Trump Administration will have no choice but to push-back...and that is exactly what we saw last week when we were out.......Things could escalate a lot quicker than the markets are pricing-in right now...epsecially if it suddenly becomes politically expedient for President Trump to push-back hard on China (even if it causes the market to decline)......Therefore, there are several reasons to think that the broad market could see some meaningful damage as we move through the rest of the third quarter. Another sharp decline in the mega-cap tech stocks...and/or a significant rise in tensions with China...might not come immediately. However, they’re both issues whose recent developments are raising a yellow flag on the broad market...and investors should take notice.

Matthew J. Maley

Managing Director

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464