THE WEEKLY TOP 10

THE WEEKLY TOP 10

Table of Contents:

1) We were wrong about August, but that does not deter our caution about September.

2) Chairman Powell’s comments last week were expected. Kaplan’s comments were quite telling.

3) An extended narrow rally means a narrow economy. Neither is good for the stock market.

4) Long-term yields around the world are rising (and their positioned to go higher).

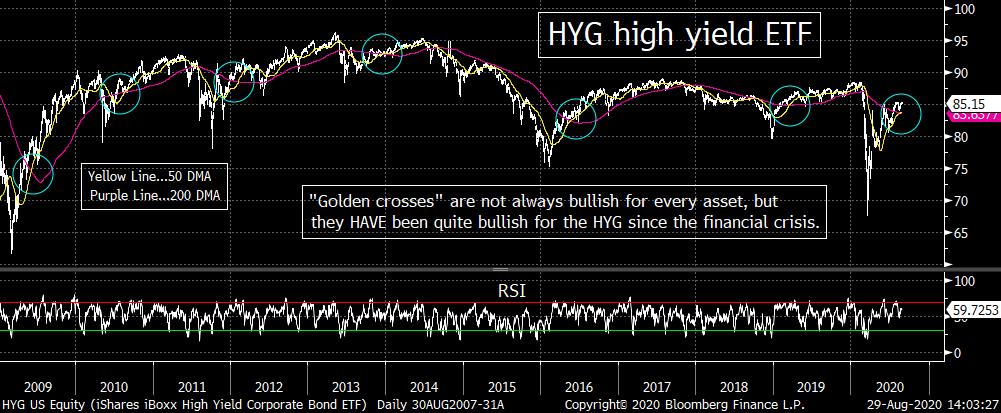

5) The HYG high yield ETF saw a golden cross last week. That’s usually quite bullish.

6) The dollar is back testing key support, but it’s still “positioned” to bounce.

7) Housing stocks (& lumber) getting overbought. Probably time for another “breather.”

8) A series of quick/short bullet points on several different subjects.

9) The Massachusetts Democratic primary results could be very telling for the November election.

10) Summary of our current stance.

Short Version:

1) Well, we were wrong when we predicted that the stock market would begin a meaningful pull-back in August. However, the market has merely become more overbought, more narrow, more overvalued and thus more vulnerable to a meaningful decline. The Fed will keep it from becoming a bear market, but the action of the past week or two are screaming “correction”...so we’re going to stick with our cautious near-term stance.

2) Chairman Powell’s comments from last week were well telegraphed in advance. Therefore, the more interesting comments actually came from Dallas Fed President Kaplan. He talked about the unintended consequences of the Fed’s moves from this past spring and that they needed to show at least some restraint going forward. This tells us that they won’t prevent normal/healthy corrections of 10% or more from taking place.....The Fed’s goal is not to push asset prices higher (like it was a decade ago). Their goal now is to merely keep stability in the markets (especially the credit markets).

3) The reasons that are being given by some pundits that narrow rallies are not warning signals are wrong. Narrow rallies are a sign of a narrowing economy...and when the economy narrows, even the best companies are negatively impacted eventually. (It also impacts their stock in a very negative way...because they become extremely overbought during a narrow rally.) Therefore, when we see a “narrow rally” over an extended period of time, it is a DEFINITE red flag for the stock market!!!

4) The yield on the U.S. 10yr Treasury note remains nears its recent highs. It’s still well below 1%, so we don’t want to make too much of this development. However, we do need to point out that the chart on the 10yr note is showing signs of a compelling bottom...and thus if it moves above 0.9% in any meaningful way, it’s going to signal that long-term rates are going higher. (Remember, the Fed controls short-term rates, not long-term ones.) With rates rising in other parts of the world...and the “positioning” in the bond market a tad one-sided, a surprising rise in long-term yields is not out of the question.

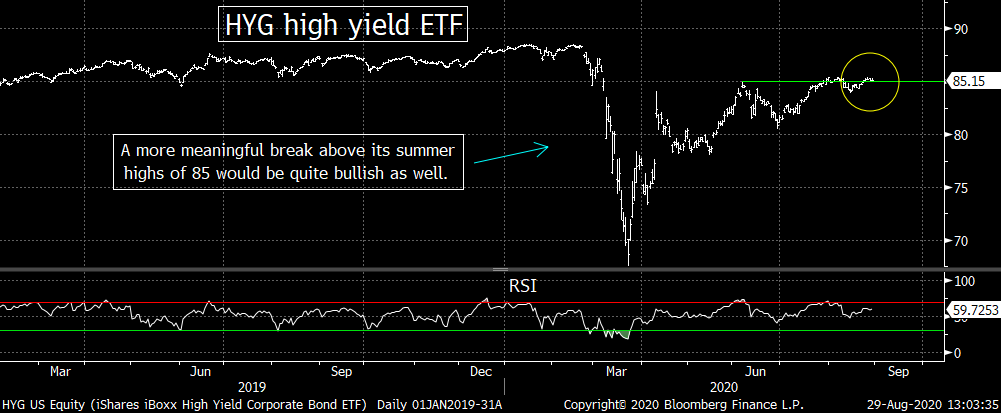

5) On the bullish side of things in the credit markets, the HYG high yield ETF saw a “golden cross” last week. Golden crosses have been very bullish for the HYG over the past decade, so this is a bullish development. We’d also not that the HYG is trying to break above its key resistance level o f $85. If it can finally break that level in a meaningful way...especially if it takes place following its recent golden cross, it’s going to be quite bullish on a technical basis.

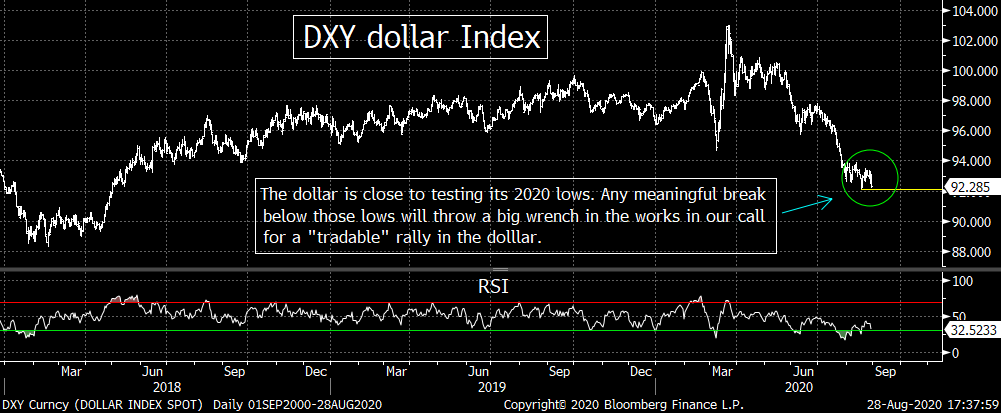

6) Our call on the dollar (higher) and euro (lower) looked quite good for a short while, but they’ve reversed back and the dollar back close to testing its recent lows (and the euro its recent highs). If they break those levels in any meaningful way, we’ll have to change our stance. However, the “positioning” in these currencies still tells us that the dollar will rally over the intermediate term...and the euro will fall. So we are not changing our stance on these currencies right now.

7) Our calls in the housing stocks have been excellent over the past two years. We remained bullish from late 2018 to early 2020. We have had to become more nimble this year...turning cautious in January and May...and more bullish in March and July. The ITB has become overbought once again...and lumber has reached its most overbought reading EVER. Therefore, this group should be do for a pull-back...or at least a “breather”...over the short-term.

8) In this one, we provide a series of bullet points...one or two sentences on several different topics. Some are related to one another...others are not. We touch on some extreme readings of bullish sentiment, layoffs at major corporations, falling consumer confidence, unjustified parabolic moves for some individual stocks, the “bear market for humans,” the belief in the American spirit...among other things.

9) Politics....The conventions are behind us, but the campaign won’t really get going until after Labor Day. However, we do have what could be a telling primary election this coming week. Believe it or not, the polls say that Senator Markey of Massachusetts is looked upon as the outsider in the primary race...vs. Rep. Joe Kennedy III, who is seen as the insider. Markey is pulling well ahead in the polls late in the game. Is this another sign that people are sick and tired of insiders...just like they were in 2016? If that’s the case, it favors President Trump................Hurrah for the NBA players (and for Tiger Woods many years ago).

10) Summary of our current stance....If it was not for the Fed ready and waiting to make sure the credit markets will not freeze up again (and another 30%+ decline in stocks would do just that), we’d be calling for a bear market right now. Instead, we’re just calling for a deep pull-back...and since the market always overshoots now-a-days, it will probably result in a full blown correction. There are just too many signs of froth today...and we’ve been doing this too long...to get sucked into buying the market aggressively at these levels. Frankly, we’re surprised that so many people who lived through 2000-2003 and 2007-2009 are getting sucked-in right now. We guess it’s just human nature to forget those bad times when things are going well. People cannot seem to help but think that “it’s different this time.” Then again, that’s what makes markets.

Long Version:

1) When we were kids, we enjoyed the show, “Happy Days”...and as much as we liked all of the characters (Marion Ross, who played Richie’s mother is a very under-rated actress) it was impossible not to love The Fonz. One of our favorite episodes was when Henry Winkler’s character was finally willing to admit that he was wrong about something, but he couldn’t get the words out. He said, “I was wr....I was wro....I was wron”...but it found it almost impossible to say the entire phrase, “I was wrong.” It was hilarious.......For many years, we have found that most pundits on Wall Street act in very much the same manner. However, we like to admit that we are wrong. We have been wrong many times in the past and we’ll be wrong again in the future.

There is no question that we were definitely wrong when we predicted that a pull-back/correction in the broad stock market would begin in August of this year. Instead, just the opposite happened...as the market continued to rally higher in an almost uninterrupted fashion. (Luckily, we still made some calls that worked out well on things like gold, the consumer staples and the currency markets.) The question right now is whether we should throw-in the towel and turn bullish...or do we continue to remain cautious.

Well, there are certainly reasons to flip and turn bullish. First and foremost is that A LOT of negative news was thrown at the market during August...and it just kept on rallying. Positive action in the face of bad news is one of the most bullish items investors can see at any given time....in any market (or in any individual stock for that matter.) The inability of our politicians to pass a new fiscal plan leads the list of the above mentioned negative news, but we’ve also had a rise in tensions between the U.S. & China, mixed economic data, continued uncertainty surrounding the election (and contested election results come November), new layoff announcements, serious concerns about back-to-school/college, etc...and yet the stock market has seen the best August for the stock market since God was a child. (Of course, that’s assuming things don’t completely fall out of bed this Monday, the 31st.)

There have also been some positive developments...led by news that we could get a vaccine earlier than the consensus had been thinking...and new treatments for Covid-19 victims that could lower the death rates for those who are inflicted.

However, as you will see from our piece today, we believe that the action in August will only make the inevitable decline worse, so we are not throwing in the towel just yet. No, this does not mean that we believe we’re going to see another major decline in stocks like we saw in Q1. The Fed is ready and willing to prevent that from happening...because they cannot afford to let the stock market create a situation that will force the credit markets to shut down again. (If that happens, the entire system will shut-down.) Yet we do not believe the Fed will keep ANY decline from taking place (and we believe Dallas Fed President Kaplan told us exactly that last week.)

The stock market is getting overbought...and the several of the small number of stocks that have been leading the market higher have gone parabolic. APPL is a GREAT company...and Tesla might rule the world some day...but that does not mean that they stock cannot (or will not) see significant declines along the way!!! The Fed KNOWS that preventing ANY decline when a market becomes expensive and overbought would not be healthy...and would cause a bubble that they could not control..........More importantly, as we will discuss today, we continue to see many signs that are SCREAMING to us that a material decline is coming for stocks in the not-too-distant future.

2) The consensus feeling about Federal Reserve Chairman Powell’s comments from last week is that the Fed will let the economy “run hotter” if the employment picture improves...because the history of the past decade tells us that full-employment is not always as inflationary as the Phillips curve has told students in economics classes for years. That said, the comments from Mr. Powell were not surprising at all...as they were well telegraphed for many months in advance...but it was seen as a further green-light for stocks.

However, we also thought that comments made by Dallas Fed President Kaplan on the same day (Thursday) were also quite instructive. Mr. Kaplan certainly confirmed the Chairman’s comments about inflation, BUT he also sent out what we thought was a decidedly cautious message about the Fed’s goals when it comes to asset prices in an interview on CNBC.Instead of stating that the goal of the Fed was to push asset prices higher (which was their stated goal for many years following the financial crisis), Mr. Kaplan warned that investors cannot rely on the Fed for asset price appreciation. He talked about the “unintended consequences” of their massive stimulus injections from this past spring. He also talked about how some of those programs would have to “sunset” (roll-off) going forward and that the Fed would have to shows some “restraint” going forward. Finally, President Kaplan said that he was very aware of the level of asset prices...which seemed to be the reason for the comments.

Fed Presidents do not follow the Fed Chairman with comments like that by coincidence. We believe that President Kaplan was sending the signal that the Fed is aware of the huge rise in asset price inflation and that they understand the damage it can do if it gets out of control. We believe this is something that should keep investors from becoming overly bullish on a stock market whose valuation has become stretched by almost every measure up at these levels...and is moving into a time frame (September) that is not always very inviting for the market. Having said this, Cleveland President Mester said that she did not think that asset prices had hit bubble levels the next day....BUT she also said that the Fed must be aware of bubble risks amid low rates. (We were going to try to attached the Kaplan interview, but when we went to the website, only the first half of the interview was available. Our apologies.)

We are not saying that the Fed is going to try to force asset prices down by any means. We’re just saying that we believe that the Fed is telling us that their goals are different than they were a decade ago. They care much more about credit market stability (instead of asset price/stock market appreciation) this time around...and that tells us that they will not necessarily step-in to prevent every little (normal) correction in the stock market from taking place.

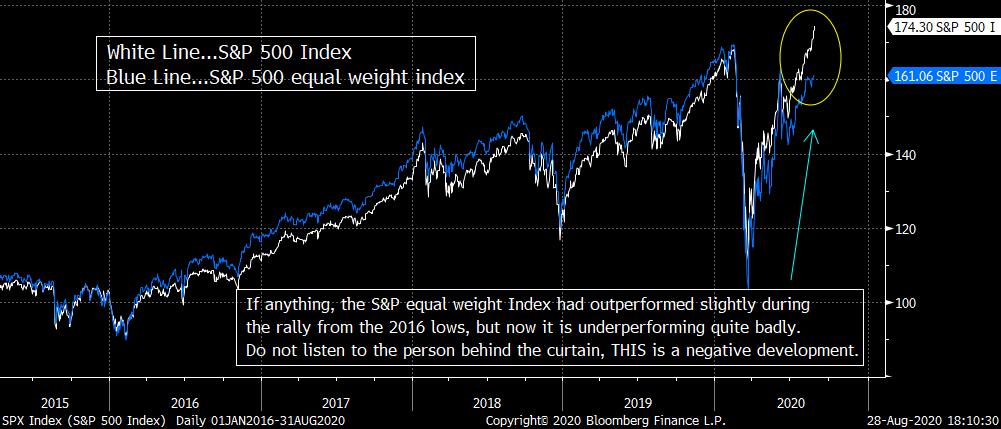

3) People are probably becoming tired of hearing how the rally has been a “narrow” one. However, we still (strongly) believe that it is important to highlight this issue...especially since the rally became even more narrow last week. Do not listen to those who say that a narrowing rally does not matter. One story says that when the market hits a new high on the same day that the breadth is negative, the market is usually higher six months later. Who cares??? When a market is making new highs, it frequently hits many new record highs within a relatively short time frame. The fact that one of those days had negative breadth...in the middle of period of strong breadth otherwise (unlike it is right now)...would mean absolutely nothing! It alsodoesn’t matter that the stock market can sometimes top-out without seeing weakening breadth before hand.

All that matters when it comes to the breadth issue is that when we get an extended rally (whether it is hitting new record highs or not)...that comes at a time when breadth is narrowing over an extended period of time (like it IS now)...it is (very) frequently followed by a meaningful decline.

The simple reason for this is that when a market rallies in a narrow fashion, it tells us that investors only have confidence in a small portion of the economy. Don’t get us wrong, there a often times PLENTY of legitimate reasons why a group of stocks (even a small group of stocks) outperform the rest of the broad stock market. However, when the divergence becomes a very strong one...especially when the rest of the market is DOWN when a small group of stocks are significantly higher (which is the situation we face today...with 5-7 stocks accounting for ALL of the gains...and net return of the other 495 stocks being negative), it signals that the broad economy is not strong enough to justify a extended rally in the broad indexes. Eventually, the rest of the market/economy has a negative impact on those small number of “leading companies”...and the stock market has to see a reset. This is especially true because the small number of leading stocks tend to become very overbought and overvalued (again, like they are today).

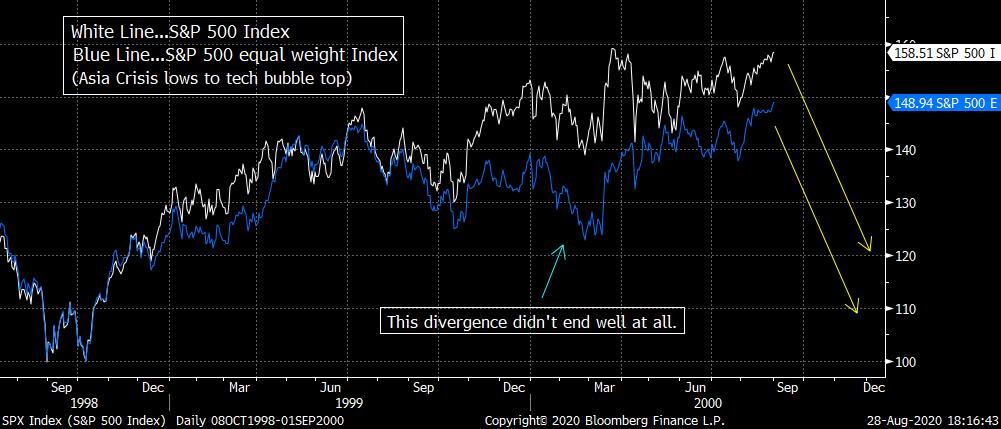

Just look at what took place in 1999-2000. Throughout most of 1999, the S&P 500 Index and the S&P 500 equal weight index traded in tandem. Then, in October of that year, they began to diverge from one another. The SPX equal weight index did try to play catch-up in the spring of 2000, but it soon faded...and the rest (as they say) is history.

4) Last weekend we touched-on the yield on the U.S. 10yr Treasury note...and how it had moved higher. We said that it was not a big deal yet because the recent rise might just be a short-term “head fake” (like it was in June)...and that we’d have to see it rise further before it would present any significant problems for bond holders (or the stock market). This is still true, but we still want to go over the technical condition of the market...because if (repeat, IF) it’s trend changes, it’s going to catch A LOT of people offsides.

Looking at the multi-week chart of the 10yr yield, it can be seen as forming a nice “base” over the past five months (and the lows from March and early August could also be seen as a “double-bottom”). Therefore, if the yield keeps rising...and pushes above the June highs of 0.9% in any meaningful way...and thus follows this nicely formed “base” with an key “higher-high,” it’s going to be a signal that long-term interest rates are going to move higher for a while. (Remember, the Fed controls short-term rates, not long-term ones.) We would also note that the trend-line going all the way back to 2018 will come-in at that 0.9% level by November. In other words, any break above that level could also take the yield above its multi-year trend line before long as well...which would make the move even more compelling!

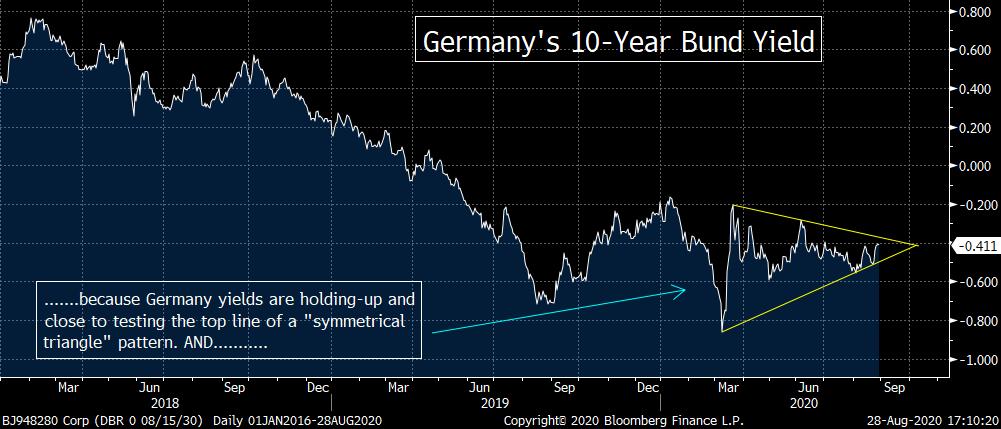

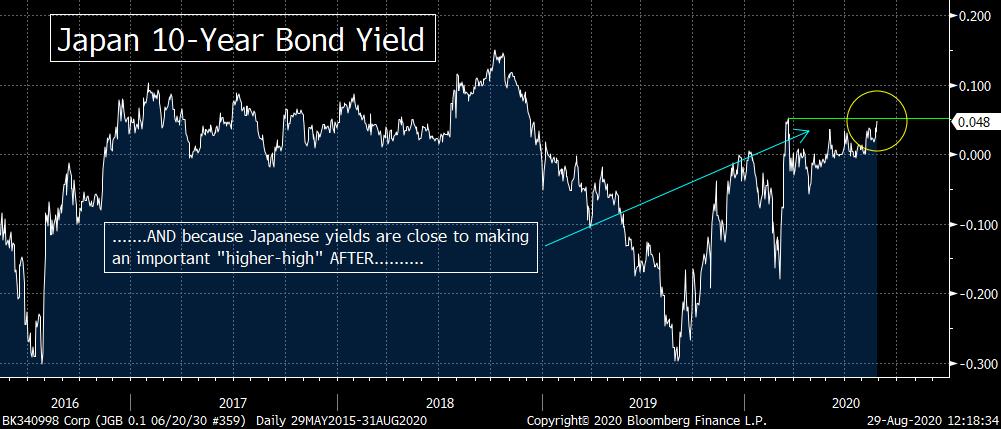

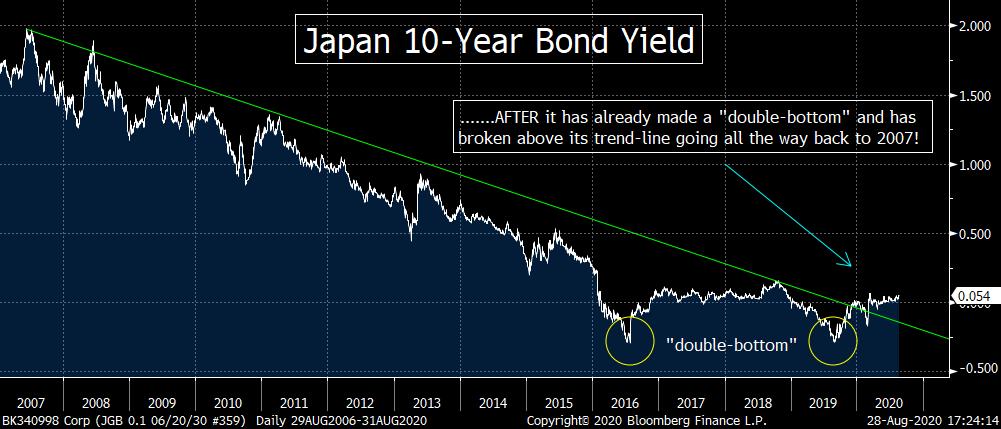

On top of all this, we’re seeing long-term rates in other parts of the world rise. The yield on Germany’s 10yr bund is close to the top line of a “symmetrical triangle” pattern, so a breakout in that market would be another surprising signal in the credit markets. Also, Japan’s long-term rates have actually been rising for a year now! They are now getting close to their March highs...so a break above that level (of 0.52%) will give it an important “higher-low/higher-high” sequence. That would be particularly compelling because this “higher-low/high” sequence would be following a VERY important long-term “double-bottom” from 2016 and 2019!!!!!

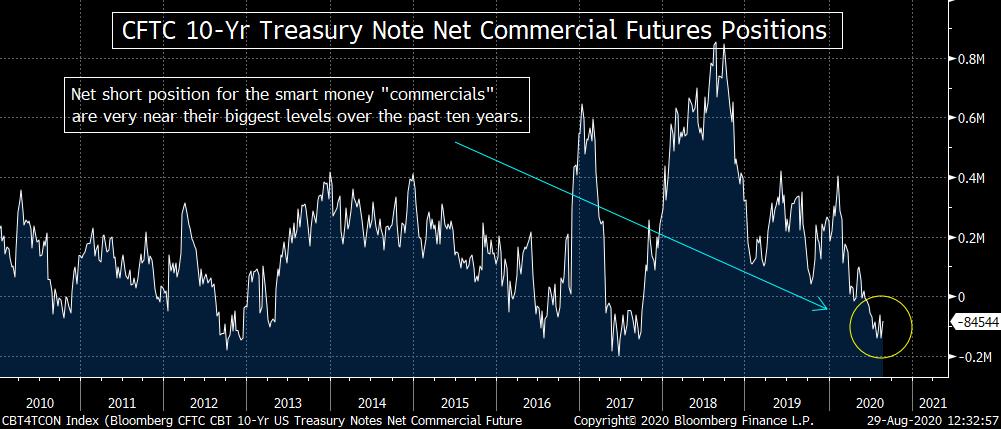

Don’t get us wrong, we still believe that it will be very tough for long-term interest rates to move a lot higher from current levels due to our concerns about further economic growth later this year and next year. However we would be remiss if we did not point out the technical situation that is beginning to developing right now...especially since the “positioning” for the U.S. 10yr note is also set up in the kind of fashion that could push long-term rates higher as well. Specifically, the COT data shows the dumb money “specs” still have a very large net long position in those longs (as we showed last week)...and the smart money “commercials” have very large short positions in the 10yr Treasury note (very close to their largest net short position in a decade). (5th chart below.)

5) Let’s switch to the bullish side of the ledger...and talk about one area of the credit markets that continue to very well...the high yield market. There are a lot of reasons to be concerned about this market...with the pick-up in bankruptcies...and the announcements of more layoffs from larger corporations. However, the announcement that the Fed would buy high yield bonds during the spring has been enough to keep this market very strong since March.

So strong, in fact, that the HYG high yield ETF saw a “golden cross” late last week. Golden crosses have been very bullish for the HYG over the past decade, so this is a positive development on the technical side of things. Now...we do have to admit the 200 DMA on the HYG is falling right now. So this development means that it was not really a golden cross the way it is usually defined. Usually, we have to see a RISING 50 DMA cross above a RISING 200 DMA. However, as we have seen at other times in the past...especially in 2016...even when the 50 DMA crosses above a declining 200 DMA for the HYG, it is still bullish.

To be honest, the high yield market scares us to death. With yields back down to 5.3%, it’s hard to call them “high yielding” instruments. And with economic growth still quite uncertain, it sure looks like a risky asset class to us. However, the HYG has been trying to break above the 85 level all summer. If it can finally break that level in a more meaningful way...especially if it can break that key resistance level following a “golden cross”...it’s going to be quite bullish on a technical basis.

(We have stated in the past many times that “golden crosses” and “death crosses” are not always a good guide. It depends on the individual stock or the ETF. For some, they are quite compelling...for others they’re not very compelling at all. However, for the HYG it does seem to be quite compelling.)

6) Our call for a surprising bounce in the dollar worked out very well two weeks ago...as the DXY dollar index bounced in a meaningful way (and it has actually flattened out over the past month). However, it fell again late last week and it is now closing-in on its August lows of 92.27. Therefore, although our call looked good on a short-term basis, we said it would be a “tradable” move that would last for several weeks. Thus if the dollar breaks below the August lows in any meaningful way, it’s going to throw a serious wrench in to the works of our intermediate-term (bullish) call on the dollar.......Conversely, any break above the August highs in the euro will also call into question our bullish intermediate-term call on that currency.

The calls we’ve made on these currencies have not been negated yet. If the dollar bounces off those August lows, our bullish call for the greenback could still workout very well. Also, the euro has formed a “head & shoulders” pattern, so if it rolls-over soon...and breaks below the “neck-line” of that pattern, it will give our call a lot of credence as well.

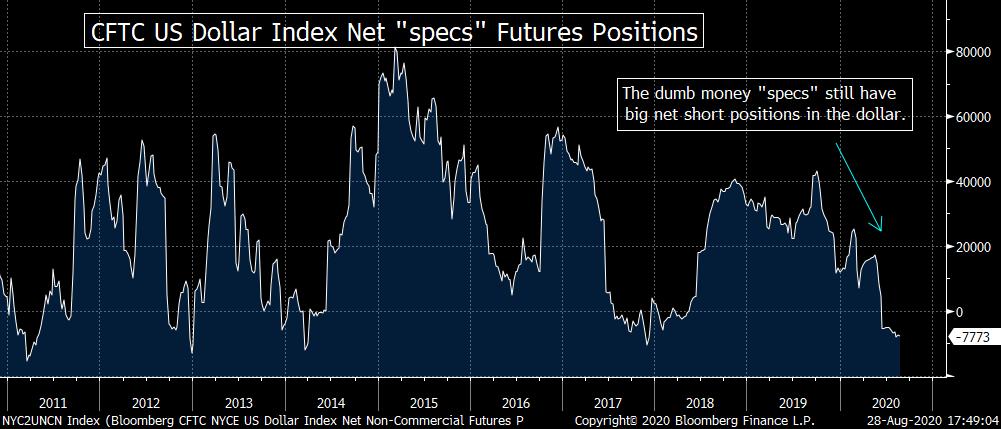

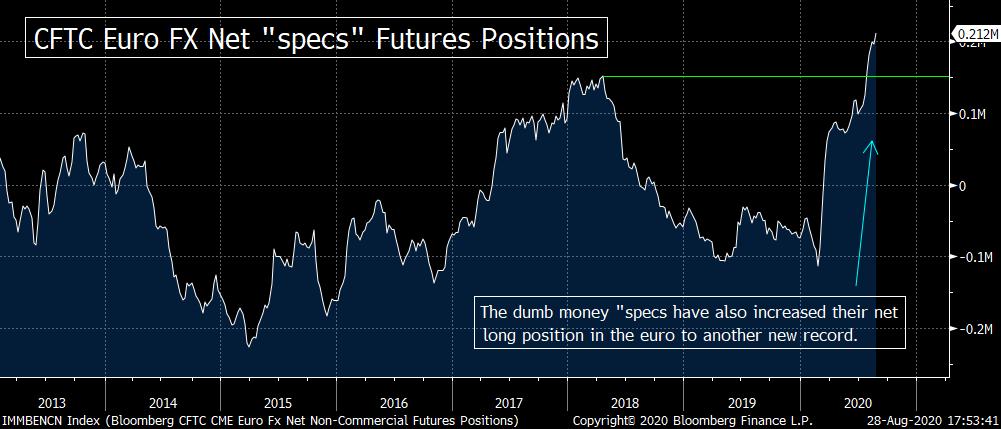

One of the key reasons why we’re sticking with our “bullish dollar/bearish euro” call is the “positioning of these currencies. As the charts show below, the dumb money speculators (“specs”) have a very large net short position on the dollar...and a record net long position on the euro. Therefore, there are too many people on one side of the boat in each of these two currencies...which will make it VERY difficult for the dollar to fall further or for the euro to rise much more. Thus we’re going to stay with our call on these currencies for now. Experience has told us that when the positions get to extremes, the markets tend to experience intermediate-term reversals...no matter what the long term fundamentals tell us they “should” do.

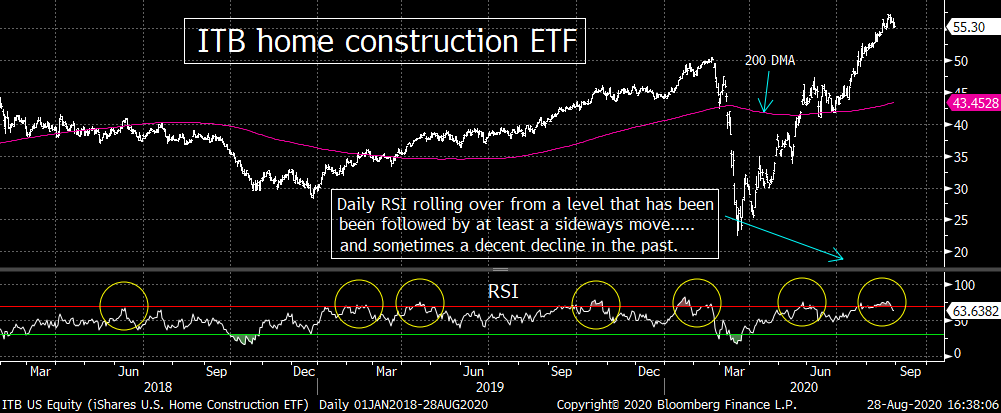

7) Our calls on the home builders continue to work out very well. We turned very bullish on the group in late 2018 and road them until early this year. We then turned cautious on the group when the ITB became extremely overbought in January. We returned to the bullish side of things for the group this spring after they (and the rest of the market) became washed out.....We then said they were ripe for a “breather” in late May (after they became overbought once again) and the group did indeed trade in a sideways range until mid-July. After breaking out of the top-end of that range, we got more constructive once again.

However, after rallying another 20% after breaking out of that sideways range...and moving 12% above their February highs, they became overbought yet again almost two weeks ago...and we turned a bit more cautious at the same time. They did rally a bit further, but the ITB is now showing signs that it is beginning to roll-over a bit...so we’re more confident now about our renewed short-term cautious stance on the group.

This is very similar to the stance we took in late May. We’re still quite bullish on the group on a longer-term basis, so we’re only looking for a short-term “breather”...rather than a significant decline. Therefore, we’re merely saying that investors should not chase the group at these levels. Instead, we’re saying that they could/should see some near-term weakness...and investors should be able to let the stocks come to them over the coming weeks.

Again, there are plenty of reasons to like the home builders over the longer-term. In fact, the group is mentioned quite bullishly in an article this weekend in Barron’s. They sighted the “tighter-than-usual supply of existing homes and chronic underbuilding of new homes”...as well as the migration out of cities and into the suburbs. They also touched on the improvement of the “move-up” market...and quoted one money manager (Bill Smead) who says, “it would take about a 1.5mm single-family homes built for about 8-10 year to meet all of the demand there is going to be”...and thus “we’re probably in the fourth inning” of this bull market in housing.

However...and as we said above...the ITB had become quite overbought recently...and the history of the past two years tells us that when the RSI chart on the ITB gets extended...AND then it starts to roll-over (like it did last week)...it’s usually a time when this group either sees a pull-back or at least takes a “breather” and trade in sideways range. Believe it or not, this has happened six other times in just the past two years, so we think this group is not going to rally a lot further over the near-term this time either. (See the RSI chart on the ITB below)

One final item to point out. Lumber has gone parabolic with its 250% rally since March and +80% in just the past month. Its RSI chart is the most overbought it has EVER been BY FAR (and the chart go all the way back to 1984).....Of course, if lumber rolls over, it won’t cause the housing stocks to tumble. In fact, the lower costs should help them. However, there is no question that these two assets are strongly correlated...and even though the home builders are not as overbought as lumber has become, they’re still overbought...and thus they could fall in tandem in much the same way they have rallied in together since March.

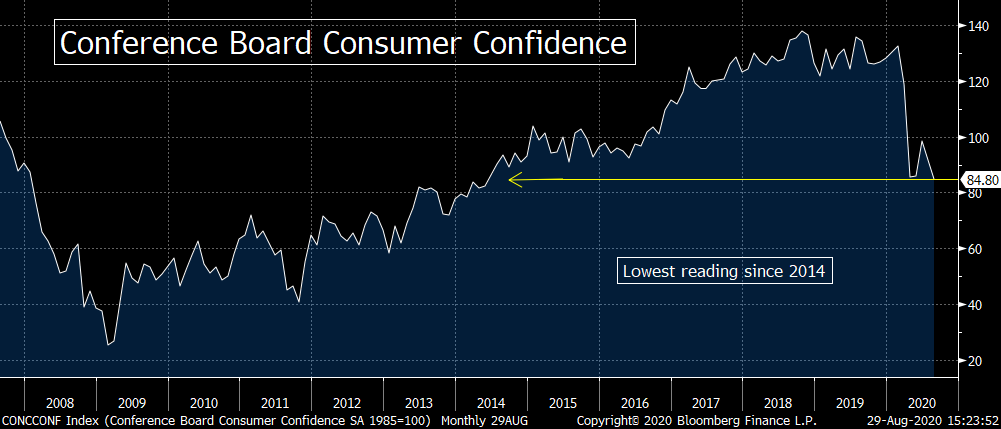

8) In this one, we’d like to provide a series of bullet points. One or two sentences on several different topics...in bullet point fashion. Some will be related to one another...others will not. Here we go: Sentiment in the Investors Intelligence data continues to get very bullish last week, with bullish sentiment reaching 60% (the highest since October 2018). The spread between bulls & bears is now 43.8 (the widest since January 2018).......KO and MGM joined BA as major corporations announcing layoffs. Look for these announcements to grow after Labor Day.......Consumer Confidence fell to a six year low in August. With no $600 checks and an increase in layoffs, this number could continue to fall. Not great for our consumer dominated economy.......Add Salesforce.com (CRM) to the list of stocks (like TSM & NVDA) which have rallied more than they should have to favorable news. Mature companies rallying more than 20% on nothing more than a better-than-expected earnings surprise is another sign of forth in the market.......Last week was the first time since 2000 that the S&P jumped more than 1% to a new high while the VIX rose more than 5%. Also, we’re told that for the first time since 2000, the S&P and VIX both rallied together two days in a row.......Goldman says that 25% of the lost jobs from the pandemic are not coming back. That leads us to highlight the scariest quote we read from this past week: “We heading towards a bear market for humans.”.......During the crisis that was WWII, Americans developed things (from all aspects of life) much faster than anyone had ever believed was possible. That should give us confidence that a vaccine for Covid-19 can be developed faster than the consensus believes during our present healthcare crisis. We believe in the spirit of America.......Ten people have died as a result of Hurricane Laura. It’s horrible that there were any deaths, but thankfully that is a very, very low number........Finally, we’re only two weeks from watching Tom Brady lead the Patriots in their opening game of the season! Oops, never mind.

9) Politics......Now that the conventions are over, the real campaign for President (and many Congressional seats) can begin...although things will probably wait until after next weekend (Labor Day) to really get rolling. That said, there WILL be one very interesting development this coming week (before Labor Day). Here in Massachusetts, the Senate primary is being held on Tuesday (Sept 1st). On the Democratic side, we have incumbent Senator Ed Markey running against Representative Joe Kennedy III (the grandson of Robert Kennedy). Kennedy had a big lead several months ago, but that disappeared over the summer...when the race became an even one. Senator Markey has pulled ahead recently...with one poll having him 12 points in the lead now.

However, as it can frequently be the case with the markets, we can learn a lot about the situation by looking at some of the “internals” of the poll. The poll (conducted by UMass Lowell) actually shows that Mr. Markey is being embraced as the “outsider wing” of the Democratic party and Mr. Kennedy (the challenger) has been seen as the insider. “This insider/outsider dynamic comes through clearly in that voters who trust government are much more likely to support Kennedy and those that distrust government are more likely to support Markey.” (You might be saying to yourself that it’s hard to think of Markey as an outsider...given that he’s been in the House & Senate for 44 years. We agree, but the polls say otherwise...and when you run against a Kennedy, it makes a little more sense as well.)

Of course, people don’t look at Massachusetts as a microcosm of the U.S. However, that’s only because it’s a VERY Democratic state

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464