Morning Comment: Imminent change in trend for the bond market?

Well, here we are, it’s September. Sure, it technically began last Wednesday, but now that Labor Day weekend is behind us, the seasonally September/October timeframe has officially begun. Of course, the fact that everybody is talking about this seasonally tough time for the market, it could very well mean that we do not run into any problems this time around. However, there is no question that we are entering the season that has experienced some scary declines in the past.

(We do want to note that although September is the worst month of the year, it’s not just September that tends to be weak. In the years when a decline in September becomes more than just a mild one, the decline usually spills into October. Thus, even though the full month of October Is usually not as bad as September, the bottom of a meaningfully rough September decline tends to last into October before it bottoms.)

Of course, there are several different reasons why the stock market sees a big increase in volatility during September. In 2001, it was a terrorist attack. However, in many cases, a rise in long-term interest rates plays an important roll as a catalyst for the decline. In fact, both of the last two corrections were followed by a jump in LT rates. In 2018 and 2020, the corrections we saw in the autumns of those years were followed by a rise in interest rates that began in August…and continued into the fall months. (We do admit that the 2018 decline did not start until early October…and last year’s correction did not spill over into October. However, these examples are merely another reason to avoid talking about ONLY the month of September when we talk about this seasonally rough time for the markets.)

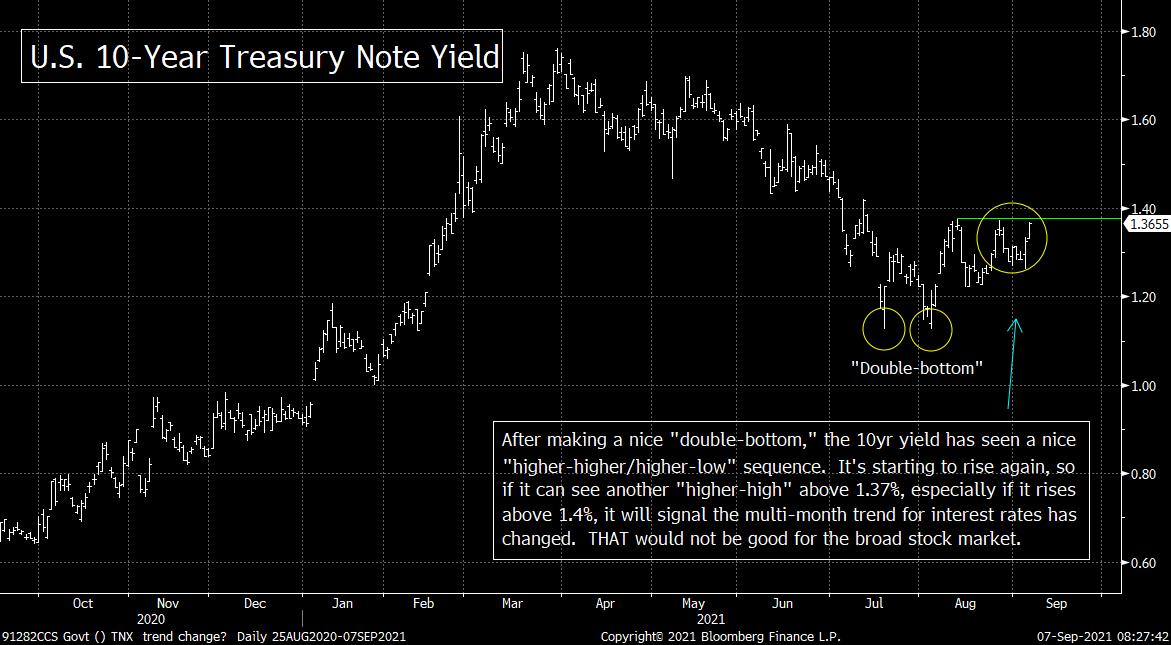

Like 2018 and last year, we have seen a rise in long-term interest rates during the month of August this year as well. The question now is whether this will continue into September (and beyond) like it did in those other two recent years when corrections began. This morning, we are seeing a rise in the yield on the U.S. 10-year note right up to the 1.37% high it saw in August (on two occasions). We have been harping on this 1.37% level quite a lot recently, but it might take a move above 1.4% to really confirm the breakout. (As we always say, a “slightly” break of any support/resistance level is not enough to confirm a breakout or a breakdown. It takes a “meaningful” move above or below those levels. Well, a move above 1.4% would make it a “meaningful” one in our opinion.)

Just to review why we believe this 1.37%-1.4% level is so important; we’ll point out that the 10yr yield made a “double-bottom” just below 1.2% in July. A meaningful break above its August highs would mean that the “double-bottom” summer low was followed by a key “higher-high” AND take it above its trend-line from May. That is the kind of move that would confirm a change in trend for long-term interest rates.

Needless to say, it might take an even bigger rise in rates to have a negative effect on the stock market. (We believe a move above 1.37%/1.4% WILLimpact the stock market, but we have to admit that it might take an even bigger rise in rates to have a materially negative effect on the broad stock market.) HOWEVER, we definitely believe that a confirmed change in trend in long-term rates will create a situation where the “rotation” within the broad stock market will return to one where value stocks outperform the growth names. Therefore, a further rise in long-term rates should have an important impact on the stock market one way or another.

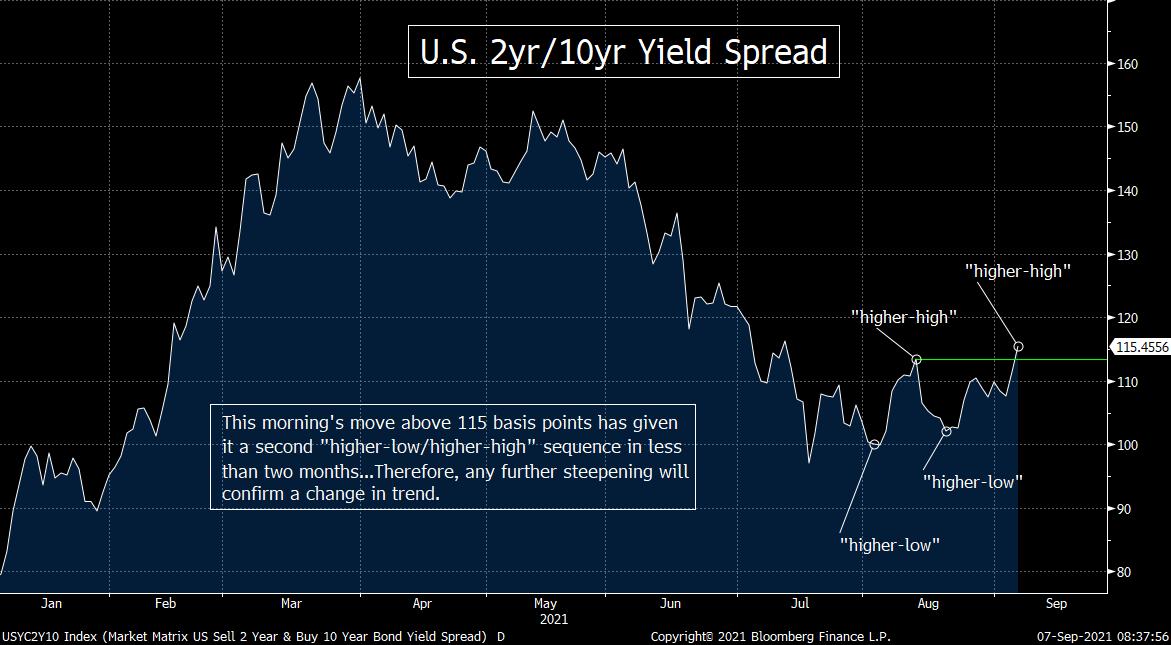

BTW, the yield curve (as measured by the 2yr/10yr spread) has already steepened to a level that has given it a “higher-high” above its August highs. It has moved above the 115 basis points level we highlighted in our weekend piece, so this is definitely a yellow warning flag for both the equity and fixed income markets……Having said this, the break above 115 basis points on 2yr/10yr spread has only been a very slight one so far. Therefore, the flag we are raising is only a yellow one…and not a red one. However, if the yield curve does continue to steepen, it will raise our concerns in a significant way. It will signal that a correction in the broad market is HIGHLY likely…and that growth stocks will almost certainly hit another rough patch.

Matthew J. Maley

Chief Market Strategist

Miller Tabak + Co., LLC

Founder, The Maley Report

TheMaleyReport.com

275 Grove St. Suite 2-400

Newton, MA 02466

617-663-5381

Although the information contained in this report (not including disclosures contained herein) has been obtained from sources we believe to be reliable, the accuracy and completeness of such information and the opinions expressed herein cannot be guaranteed. This report is for informational purposes only and under no circumstances is it to be construed as an offer to sell, or a solicitation to buy, any security. Any recommendation contained in this report may not be appropriate for all investors. Trading options is not suitable for all investors and may involve risk of loss. Additional information is available upon request or by contacting us at Miller Tabak + Co., LLC, 200 Park Ave. Suite 1700, New York, NY 10166.

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464