THE WEEKLY TOP 10

We just want to make a quick comment because we have some new readers. Each point begins with a very quick summery (in bold letters) of what we’ll say in the “body” of that bullet point. We still like to use bold letters in other parts of the text to emphasize a point, but we just want to make sure new readers know why what we say after the first paragraph can sound a bit repetitive…..Thank you.

THE WEEKLY TOP 10

Table of Contents:

1) There’s no question that the last 2 QE programs have helped the stock market rally strongly.

2) When QE creates the “building up of leverage”…less QE creates the “unwinding of leverage.”

3) Stagflation is becoming more and more evident every week.

4) Suddenly, the outlook for earnings is not quite as strong as it has been for most of this year.

5) It’s not just the airline stocks, the railroads and trucker have been weak lately as well.

6) The CRB commodity index is close to breaking a key resistance level.

7) Declines of 4% do not create “great buying opportunities.”

8) U.S….China….Taiwan…….The situation continues to get more complicated.

9) Remembering 9/11……So many heroes.

10) Summary of our current stance.

1) The ECB announced last week that they are going to begin to taper back on their bond buying program by the end of the year…and we got more evidence that the Fed is VERY likely to start tapering on their own massive bond buying program before the end of the year as well (even if they don’t announce it in September)….We can argue whether this will have a negative impact on the markets or not, but one cannot argue that the Fed’s last two QE programs have helped the market rally strongly since September 2019. (That’s right…September 2019, not March 2020.)

On Thursday, the European Central Bank announced that they were going to cut the level of their monthly bond purchases. Of course, the ECB said it is not “tapering.” (This is very similar to what the U.S. Fed said in the fall of 2019 when the repo market fell into disarray. They said it was not a “QE program.”)…….The ECB is trying to claim that since it will be a single cut back…and will not accelerate every month…it is not a “taper” move. However, they’re merely parsing words. They ARE tapering…just like the Fed DID engage in a QE program in the fall/winter of early 2019. In other words, there will be less liquidity in the global system as we move through the rest of the year…just like there was MORE liquidity in the system over the last 3-4 months of 2019.

We also heard from several different members of the U.S. Fed last week (Williams, Dudley and Bostic) who all confirmed that the Fed IS going to start tapering back on their own bond purchases before the end of the year (even if they don’t announce it in September). They all said it was time to taper…and Mr. Williams (the President of the NY Fed…and thus the second most important member of the FOMC) said that they’ll “taper” even if the rate of job growth slows somewhat over the rest of the year.

In other words, unless another emergency raises its ugly head soon, two major global central banks are going to be providing LESS liquidity later this year (and into next year)….in the exact opposite way that the U.S. Fed provided MORE liquidity in late 2019. Therefore, this should create a situation at some point soon where the stock market does the exact opposite of what it did in the last 3-4 months of 2019. (The stock market should begin to correct due to this lower level of liquidity…in just the opposite manner that the stock market rallied in the final months of 2019 in reaction to the increase in stimulus.)

Having said all this, we admit that these moves by the Fed & the ECB might not create an immediate catalyst for a decline in the stock market. However, it will make it MUCH HARDER for the market to shake-off other new developments…like it has for most of this year.

2) If you look at 2013, the Fed provided less stimulus in 2013 with their “taper” program that year…and the stock market barely fell at all. So why are we concerned? In fact, after a very mild drop, the market resumed its rally before the end of the 2013, so why would the stock market decline this time around? Well, the stock market is much more expensive than it was in 2013. However, the MUCH MORE IMPORTANT issue is that there is A LOT more leverage in the marketplace today.

Wait a minute! If you look at 2013, it should take away any of the concerns we raised in point #1! The Fed provided less stimulus in 2013 with their “taper” program that year…and the stock market barely fell at all. In fact, it resumed its rally before the end of the year, so why would the stock market decline this time around?

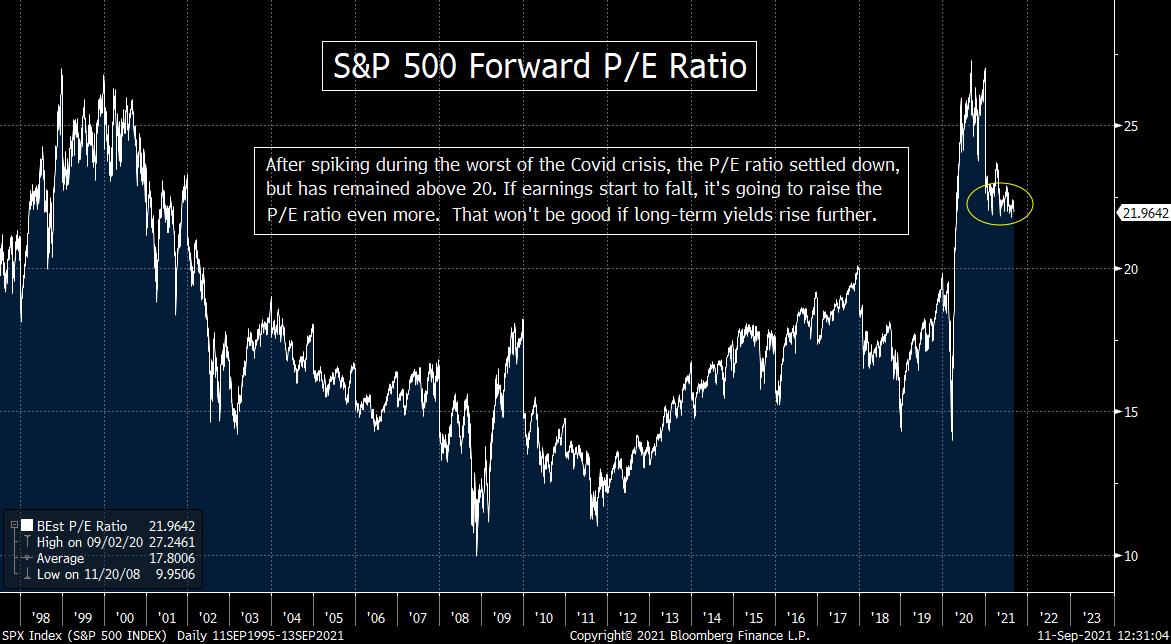

Well, first of all (and as we’ve stated several times in recent weeks), the stock market is MUCH more expensive than it was back in 2013. The S&P 500 is trading at better than 22x forward earnings and over 3x sales…vs. about 15x forward estimates and just 1.5x sales in 2013.

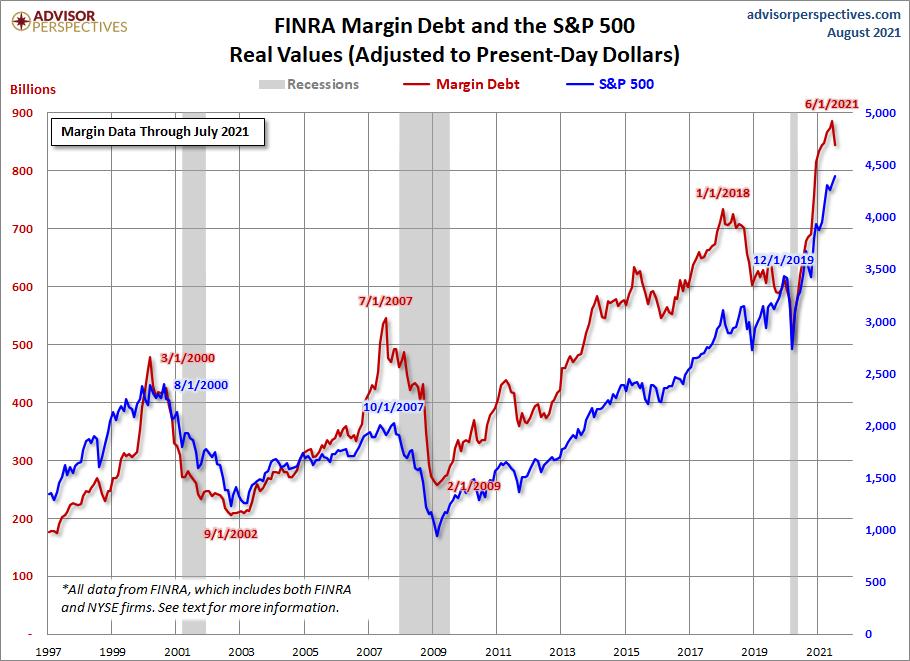

However, this is another VERY important reason why the market will likely have to drop now that the global central banks have decided to pullback on their emergency levels of stimulus: The level of leverage in the system a MUCH, MUCH higher than it was in 2013. Margin debt as of the end of July (the last month of the data is available) is than 120% higher that it was in July of 2013!!! ($844bn vs. $382bn in 2013!)……With less liquidity coming into the system each month, at some point, at least some of that leverage is going to have to be unwound. THAT will will create some serious headwinds for the stock market…NO MATTER HOW FAR OUT the Fed pushes out their decision to start raising short-term rates.

We (strongly) believe that the “winding up of leverage” has played a bigger role in the continued rally off the March 2020 lows than most people realize. This has been especially true this year…after the emergency in the economy had passed. (No, we do not think that monetary stimulus is the ONLY reason the stock market has rallied so strongly. We just believe that a good-sized portion of the rally has been driven by this liquidity.)

Yes, it’s great that earnings have been so strong this year. However, they’re still only about 23% higher on the S&P 500 than they were in both 2019 and 2018. That might sound good, but the stock market stands about 40% above its closing level from 2019 and 80% above its closing level from 2018! (It’s about 50% above its mean level from 2019 and about 65% above its 2018 mean level.) So, as you can see, the stock market has improved much more than the fundamentals have improved since 2018 & 2019.

This is why the P/E ratio has reached such a high level…and why the price-to-sales ratio is at a RECORD high level. We believe it also shows that the MASSIVE emergency levels of stimulus that was thrown at the financial system has played an important role in the degree this market has rallied in such a strong way over the past 18 months. (As the economy moved out of its emergency situation…and the emergency level of liquidity just kept on coming…and that has pushed the stock market well above anything that can be justified by the fundamentals in our humble opinion.)

We would also argue that this persistent emergency level of stimulus…that continued to pour-in even though the emergency had passed…is a key reason why the market has been able to continue to rally in an uninterrupted way for much of this year…even though it has had plenty of reasons to see a material pull-back on several occasions……As this really has continued uninterrupted, it has also given investors the kind of confidence to add more leverage to their positions. This, in turn, has helped the rally feed on itself.

In other words, the “building up of leverage” that has helped this market rally so strongly is coming to an end…and as that stimulus/liquidity becomes less plentiful, the “unwinding of leverage” will create some material head winds for the stock market in 2022……In fact, we believe those headwinds could come very soon…before we get to 2022. (Remember, as we pointed out last weekend, an extreme level of high margin debt only becomes a problem when it falls in a meaningful way. So far, it has only declined slightly, but…..)

Source: Advisor Perspectives

3) We continue to get more evidence that the issue of “stagflation” will become a problem going forward. (In fact, it might be better to say that stagflation will become a bigger problem…because some are saying that we’ve already entered a stagflation phase.) Either way, it’s an issue that is certainly getting more traction.

We received some more evidence last week that “stagflation” will become a much bigger problem in the months ahead. Some people say that it’s already a problem. Most pundits would agree with this, but some of them believe that it will be “transitory” because they think the inflation part of stagflation will be transitory. However, there’s little question that both the “stag” part…and the “flation” part…of “stagflation” seem to be getting worse right now.

On the “stag” side of “stagflation,” we’ve seen weaker-than-expected data on the employment front, the housing market, retail sales, etc….over the past two weeks. No, the data is not pointing to a significant slowdown (much less a recession), but it does show that the expectations for growth in the second half this year are going to be weaker than the stock market has been pricing-in…and maybe in 2022 as well. Last week, we saw several major Wall Street firms (including Goldman Sachs & Morgan Stanley) lower their expectations for growth over the rest of this year…and it probably won’t take much more weak data to cause them to start lowering expectations for the early part of 2022.

On the “flation” side of “inflation,” we saw a higher-than-expected PPI number on Friday here in the U.S.…and earlier in the week, China announced that their own PPI data in August came in at a 13 year high of 9.5%! Therefore, it is becoming more and more evident that inflation around the world is not going to be as transitory as the Federal Reserve has been saying this year.

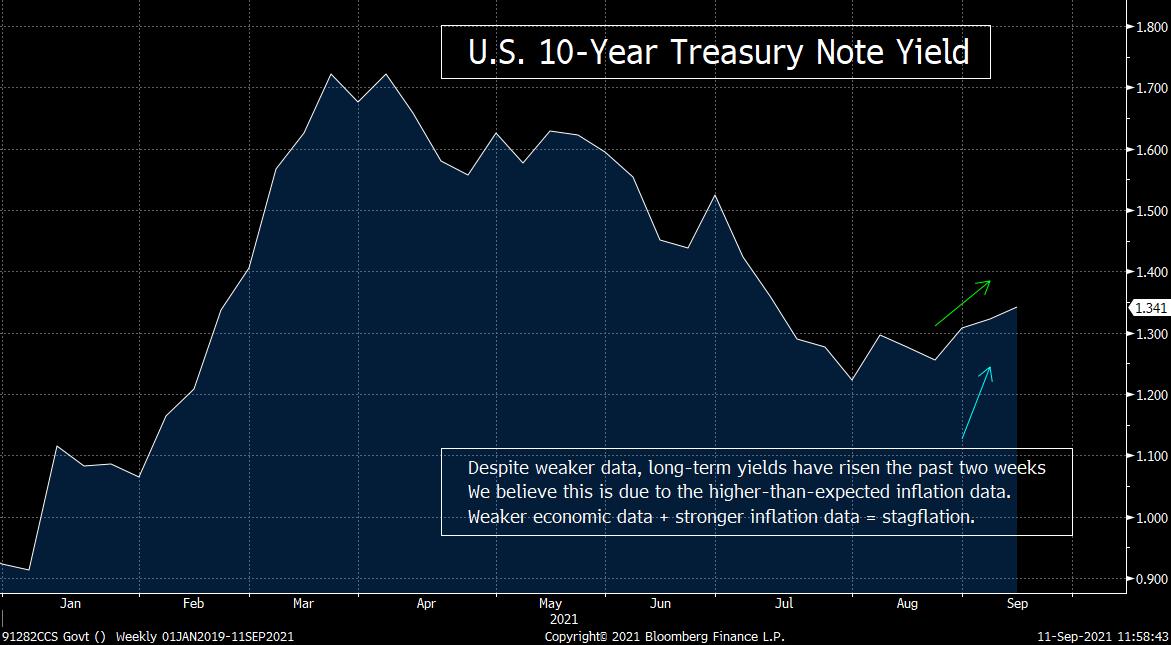

All we have to do is look at the bond market. We had the above-mentioned weaker-than-expected numbers over the past two weeks (led by the weaker than expected employment report), and yet the yield on the U.S. 10-year note has risen from 1.26% to 1.33% over those two weeks.

We still think that the yield on the 10yr note has to rise above the August highs of 1.37%...and likely above 1.4% to confirm the breakout…but if/when that takes place, it’s going to also confirm a change in the multi-month trend in bond yields to the upside. If that continues to take place at a time when the data is not strong (and Wall Street firms keep cutting projections), it’s going to be an even clearer signal that stagflation is indeed going to be a problem going forward.

4) If the variants of the coronavirus…or any other reason…causes the economy to slow further as we move towards the end of the year and into next year…what kind of impact is that going to have on earnings? Earnings have been GREAT so far this year, but they’re expected to remain on a sharply higher trajectory for the rest of this year…and next year. If this trajectory starts to flatten out, it’s going to create headwinds for this very expensive stock market.

Not only are we hearing reports that several big Wall Street firms are cutting their economic forecasts, but we’re also staring to hear concerns about the level of earnings forecasts. BofA highlighted last week that the pace of earnings growth so far this year is showing signs of stalling. They sighted the “guidance ratio”…and it is beginning to roll-over. We do admit that the guidance ratio stood at a record high four weeks ago, so the fact that it is falling a little bit is not enough to signal that we’re about to see a big change going forward. However, there are some other developments that bolster this argument.

For instance, the airline industry lowered guidance across the board late last week…sighting a lower level of bookings for the rest of this year (including the holiday season)……On top of all this, companies like PPG and SHW cut their outlooks for the current quarter this past week…sighting rising raw material costs and higher costs due to supply chain issues. PHM sighted similar issues when they cut their forecast as well. We’d also note that GE sighted the chip shortage that has been plaguing the auto industry when they warned that they might have to lower guidance.

Again, this evidence is not enough yet to say that earnings growth is going to slow in a material way…or that the slowdown will last very long even if it does take place. However, we keep hearing how the high valuation levels we’re seeing today are justified by the extremely low interest rates. Well guess what, those interest rates are starting to rise again…and the level of earnings growth is showing signs of fading. That does not bode well for a stock market that is trading at 22x 2021 estimates.

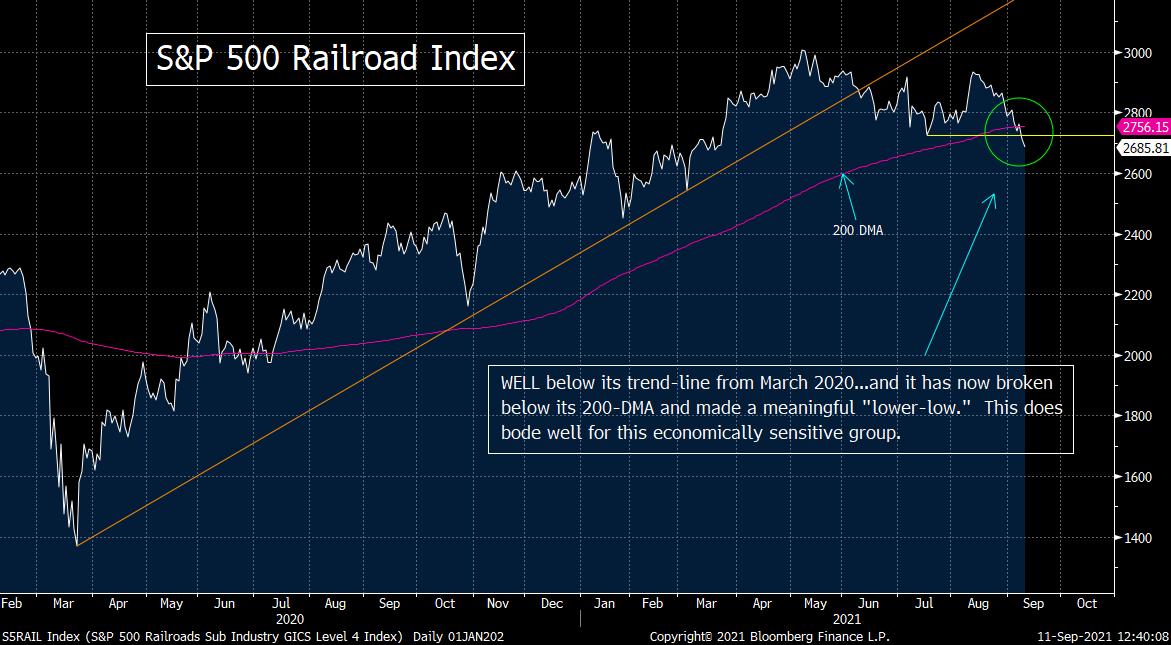

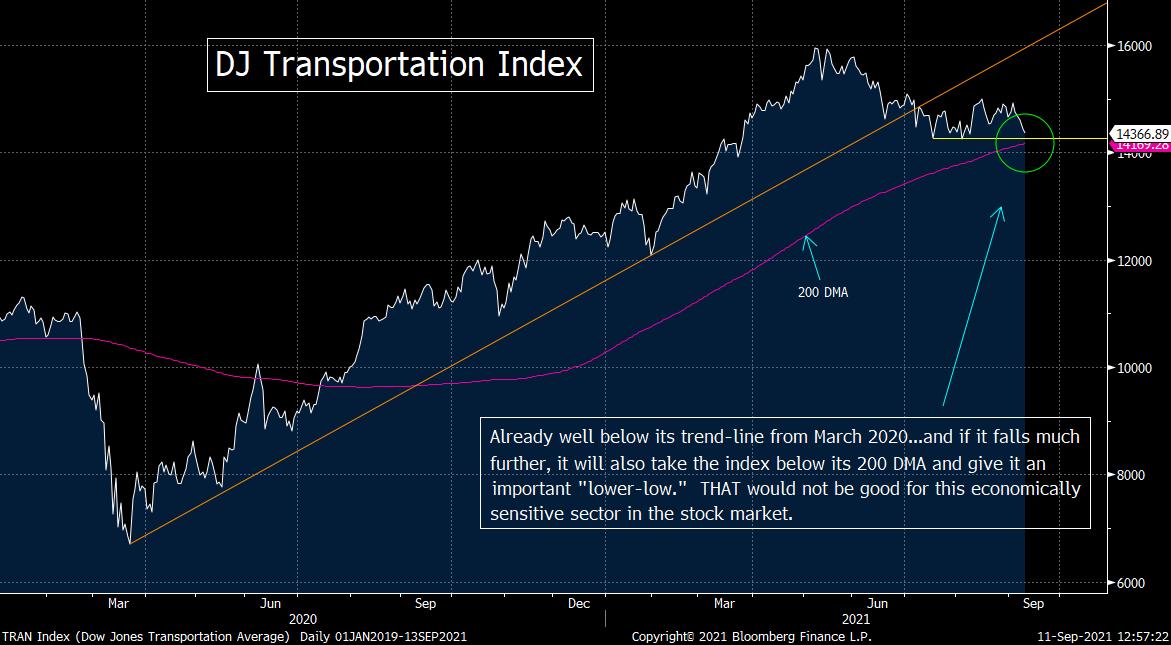

5) One sector that is also signaling that we could be in for a rough patch in the economy and/or earnings for more than just a few weeks and months is the Transportation sector. Not only are the airlines making negative announcements (and acting poorly), but the very economically sensitive railroad and trucking groups are also not acting well at all. If these groups fall further, they will break some very important support levels. The same can be said about the broad DJ Transportation Index.

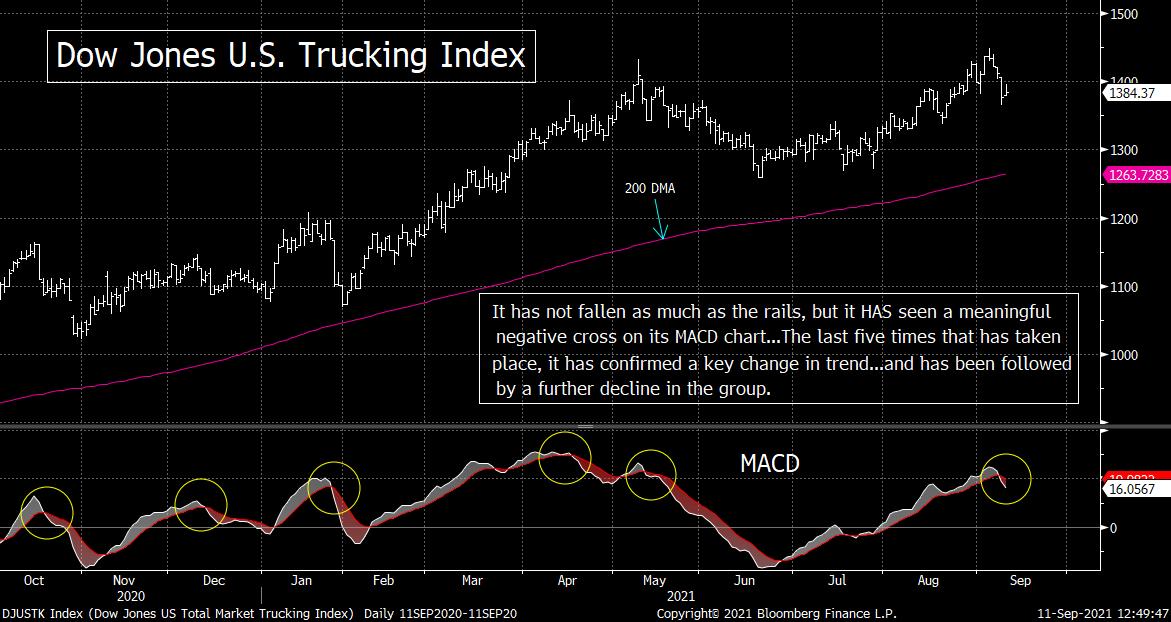

The action and recent news in the airline group has taken attention away from the poor performance of other groups within the broad transportation sector. The S&P 500 Railroad Index fell into correction territory last week and now stands 10.5% below its May highs. The Dow Jones U.S. Trucking Index has rolled over more recently…and is now 4% below its summer highs.

In fact, the railroad index had now broken WELL BELOW its trend-line from March 2020…and last week’s drop took it below its 200-DMA (for he first time in over a year)…AND gave it a key “lower-low.” This is very negative on a technical basis for this important economically sensitive group.

As we mentioned, the decline in the truckers is a more recent phenomenon, so that index has not broken any key support levels yet. However, it did see its first compelling negative cross on its MACD chart since May. That negative “cross” in May was followed by further decline that led to a more than 10% drop from the highs. In fact, it has been followed by a significant decline each of the last 5 times the index has seen a meaningful negative cross. Therefore, even though this group has not been as weak as the railroads, its MACD chart is telling us that it has lost a lot of momentum.

As for the broad DJ Transportation Index, it fell below its trend-line from the March 2020 lows in June. Unlike the railroad index, it has not yet broken below its 200-DMA or made a key “lower-low” below its summer lows. However, it’s not far from doing just that. If the TRAN falls below the 13,800 level in any substantial way, that would do the trick…and it would confirm an important change in trend has taken place for this very important economically sensitive sector of the economy/stock market.

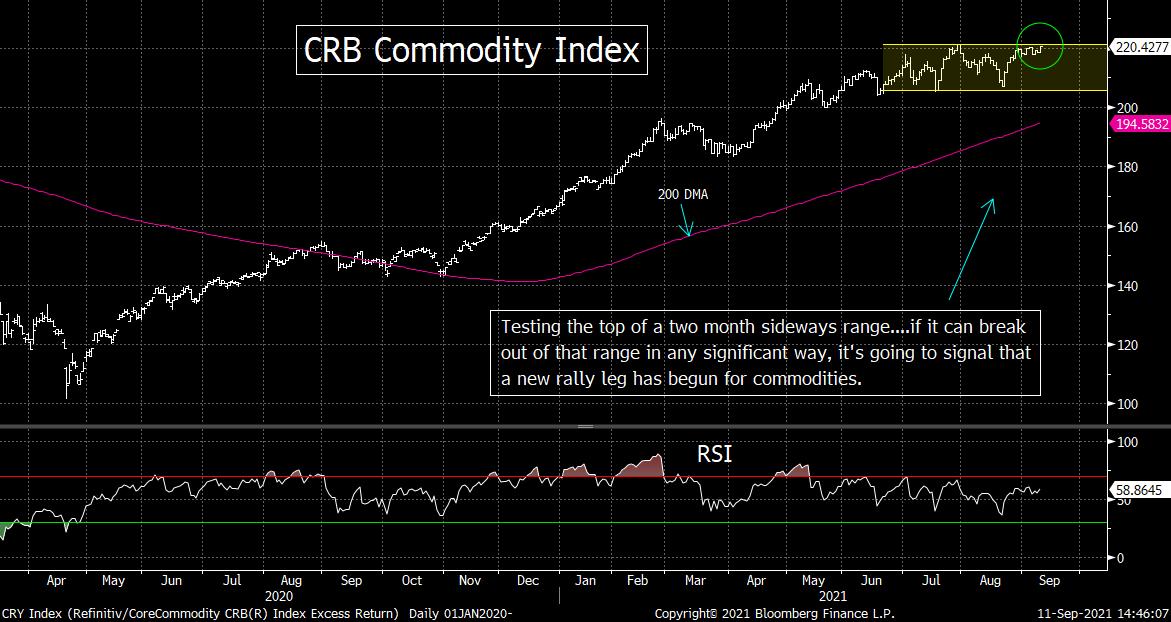

6) As we highlighted in an earlier bullet point, the inflation data is rising. This is taking place even though we’ve seen some weakening of the economic data. However, what about commodity prices? Well, despite the fact that lumber saw a huge decline from May into July, commodity prices continue to rise. In fact, the CRB Commodity Index is testing a key resistance level. If it breaks-out from here, it will be another reason to think inflation will not be very transitory.

The more than 70% decline in lumber prices from May into July of this year got a lot of headlines. However, that still left the price of lumber at a much higher price than its average over the past 10 years. Also, lumber has stabilized a relatively high level (compared to the last decade) over the past two months.

We’d also note that “Dr. Copper” has rallied 10% over the past 7-8 weeks (after a very nice bounce off its 200-DMA). Crude oil has also bounced nicely in recent weeks…and it did not fall after China announced that they’d release some crude oil from their strategic oil reserves for the first time ever! On top of this, natural gas has rallied over 30% recently…and now stands at its highest level in seven years!

Okay, now let’s look at the CRB Commodity Index. This broad index for the commodity asset class has more than doubled since the pandemic lows of March 2020. However, the index did flatten-out for a while in the second half of the summer. Now, however, its rebound of the past few weeks has taken it up to the top line of its sideways. Therefore, if it rallies much further from current levels, it will signal an important “breakout” for commodities…and indicate that a new rally-leg has begun. Needless to say, that kind of move would put a big dent in the Fed’s argument that inflation is going to be transitory/temporary.

7) As we’re sure you’ve all heard, Apple Computer (AAPL) received a negative ruling in their antitrust case with Epic on Friday. This knocked the stock down by more than 3% on Friday. On the technical side of things, the decline did not do any important damage to its chart. However, we question whether this drop has provided a great opportunity to buy the stock. This does not mean that the stock cannot bounce-back quickly. However, some pundits are trying to portray it as a “great buying opportunity.” THAT is a BIG stretch…and it tells us that there is a lot of complacency built into this stock.

AAPL Computer (AAPL) is a GREAT company. In fact, back in June of 2019…after the stock had dropped 18% over just three weeks…and when many on Wall Street were saying that AAPL was losing its luster in a major way (because they were “no longer the innovator they were under Steve Jobs)…we started pounding the table saying it was a great buying opportunity! We talked about its service business…and the massive amounts of cash the company garnered every quarter. The stock has rallied almost 250% since we made that call just over two years ago, so it has worked out quite well.

On Friday, the company received a negative ruling in their antitrust case with Epic…and the stock fell 3.3% on the day. This left it less than 5% below its all-time highs…and yet we hear that some pundits are trying to say that this is another “great buying opportunity.” They say this ruling is really not a very big deal. We have also heard some say that the stock is oversold and the entire tech sector is also oversold…and thus this is a great time to buy the stock/group.

We’re sure you will hear/read many opinions on whether this news will have a material impact on AAPL’s prospects by the time the market opens again on Monday, so we won’t step into the middle of that discussion. (Besides, we do not cover the stock, so our comments would only be general in nature…much like they were in June of 2019.) However, if you look at the chart on the stock, it is NOT oversold at all (and neither is the tech sector in general). Therefore, this very mild decline does not provide a “great buying” opportunity in our opinion.

We do need to note, however, that we are not saying that the stock will definitely fall a lot further before it rebounds. Let’s face it, their iPhone 13 announcement next week could be a catalyst for another big bounce…..We’re merely saying it could fall further…and we strongly believe that those who say that the stock is oversold on a technical basis are quite wrong. (It wouldn’t be accurate to say that about the tech sector in general either.) We’d also say that if the iPhone 13 announcement is not a bullish catalyst, it won’t take much more downside follow-through for it to be a very negative development on a technical basis.

Again, AAPL is a great company…and the stock has been a fabulous over the years. However, it’s going to take a MUCH bigger decline for this stock to be oversold enough (and cheap enough) to be seen as a “great buying opportunity.” When a stock has rallied 35% in less than 6 months…180% in 18 months…340% since the beginning of 2019…and stands at an expensive level on an historical basis…a decline of 4.9% can hardly be called a “great buying opportunity.”…..Heck the stock has rallied almost 5,000% since the financial crisis lows of early 2009, but it has still seen 27 corrections of over 10% since those 2009 lows…and 12 declines of more than 15%. (Some much more than 15%.)

8) At the beginning of the year, we said that that the most important geopolitical issue facing the world in this decade will be the tensions between the U.S. and China…and that China’s desire to bring Taiwan back into the fold would be at the center of this conflict. The tensions between our two countries have only grown over the past 8-9 months. This does not mean that anything will come to a head over the next few weeks or months, but this issue sure ain’t going away either!

In an interview last week, investor Kyle Bass said that he thought that China would make a move on Taiwan within the next year or two. Geopolitical experts have been worrying about a move like this by China at some point under Xi, but most have been saying that China was playing the “long term game” and wouldn’t make a big move for several years (at the earliest).

We’re not sure why Mr. Bass believes this could now be an imminent threat. Maybe it’s because the Biden Administration handled the Afghanistan transition so poorly, that it has emboldened China to make a move more quickly (under a perceived weak president)…..Khrushchev made a move in Cuba after the Bay of Pigs disaster made Kennedy seem very weak. Thus, maybe Xi will try to do the same thing sixty years later. Xi is likely to think that China can be much more successful than the Soviets were during the “Missiles of October” crisis…given that Cuba was in our back yard and Taiwan is halfway around the world.)

Okay, we are not experts on geopolitics, so we have no idea if Mr. Bass is correct or not. What we do know is that the tensions continue to rise between our two countries. Taiwan held war games in August. Japan seems to be worried more about the conflict…as they are now publicly linking any attack on Taiwan to Japan’s own national interest. These comments from Japan caused China’s Foreign Ministry express “strong dissatisfaction and firm opposition” to Japan’s remarks. This is somewhat similar to what Xi himself has said this year after comments from other global leaders (including those from the U.S.)…when he said, that those who interfere with China’s plans for Taiwan will “get their heads bashed bloody.”

When you combine these developments with the fact that China has continued to fly military planes in Taiwan’s airspace…and reports that the Biden Administration renewing trade tensions with China by weighing a new investigation into Chinese subsidies and the impact that might be having on the U.S. economy…it’s not a good situation. Those flights include an incident this past week…when 19 nuke bombers and fighters flew into Taiwan’s airspace during what the called “invasion war games.”

Again, we cannot predict when this situation will become a red-hot one. However, you do not have to be an expert on geopolitics to know that a DEEPLY rooted goal for China’s government is to bring Taiwan back under their direct control. You also don’t have to be an expert to know that Xi wants to make sure this takes place while he is at the top of their government. Xi Jinping is not even 70 years old, so it’s not like he would need to rush this process. However, the situation is getting worse at a much faster pace than people were thinking at the beginning of the year. Therefore, it’s something we all need to keep an incredibly close eye on over the coming weeks and months.

9) We cannot finish this weekend’s piece without acknowledging the 20th anniversary of 9/11. We were not in NYC that day, so we cannot pretend to understand what those who lived through the horror of that day went through. However, it was still a day that is etched in our memory…as it is for every American who is old enough to remember that day. We will always remember the people who died on 9/11…and we will always honor those who answered the call for help.

When I was in my 20’s, I used to wonder if there would be a day when everyone from my generation would say, “I remember where I was when….” For my parents, it was the bombing of Pearl Harbor. For those who were a bit older than my parents, it was the day that President Kennedy was shot in Dallas. For me, the tragedy of the Challenger disaster was something that I remembered quite vividly, but I knew that there was likely going to be something else that would be that ONE historic day I would always remember.

To be honest, my story from that day is not very interesting. Like I said, I was in Boston, not New York. I do remember thinking that the first crash into the towers could not have been made by a small plane (as was originally reported). The hole was too big. Then, when the second plane hit, we all knew that it was not an accident.

I was working at Merrill Lynch at that time. The Head of Equity Trading in NY…Ed McMahon…was away from the office downtown when the planes hit, but he saw what had happened as he headed back to the Merrill offices (which were very close to the towers). He did not wait to hear from anyone above him. He came into the building and immediately went onto the massive trading floor and picked up the “squawk box” speaker-phone and told everyone to leave the building. Like so many New Yorkers that day, Eddie kept his head…and made the right decision. I don’t know if his decision saved a lot of lives, but he definitely enabled hundreds of people in the Merrill downtown building (that was eventually BADLY damaged when the towers later collapsed) to get out safely…and without any panic. (In other words, he probably DID save lives…and at the very least, he definitely kept A LOT of people from being injured.)

Eddie would be the first to say that there were hundreds of New Yorkers (especially from the NYPD and NYFD) who did things that were much more important than what he did that day. However, Ed…and many leaders like him…still did things that made a big difference on 9/11. As bad as things played out that day, it could have been even worse.

Anything else I say about what I remember about 9/11 will pale in comparison to what those who were actually in downtown NYC that day could tell you. Therefore, I will leave it there. I will only add that it was a day that brought out the best in America over the following days, weeks, and months. Hopefully, the 20th anniversary of this tragedy will help us remember what we can do when we come together…and thus it will help us reverse the move towards a much more divisive society that we’ve been experiencing over the past decade or more……Finally, may God bless the lives that were lost on 9/11…and God bless those who lost loved ones and continue to suffer from that horrible day in history.

10) Summary of our current stance…….In the 17 months since the stock market bottomed in March of 2020, the S&P 500 Index has rallied almost 75%...and it has only seen three negative months. January of this year….and September & October of last year. That is pretty darn amazing.

We could give you a bunch of trivia that tells you what happens to the stock market when it rallies strongly for more than a year…with only a couple of down-months…but those facts really won’t mean much. (The bulls will tell you that it means the momentum is strong and thus it is signaling further gains to come. The bears, in turn, will say that the market can’t keep up this pace and thus we’re do for a correction.) However, since we’re in the middle of a truly unique situation, we don’t think these numbers (in-and-by-themselves) mean a whole lot.

One of the main reasons why this is such a unique period in our financial history is because of the massive monetary stimulus that has been provided to combat the global healthcare crisis. However, both the U.S. Fed and the ECB have told us that they are going to cut-back on their emergency-level stimulus programs in the very near future. No, it might not happen immediately, but it’s coming VERY soon. Therefore, even if this development does not cause the markets to decline, it will make it much, much harder for them to shake-off bad news to the degree they have been able to do for all of this year.

The one piece of “bad news” that does finally provide the catalyst for a correction could be anything. It could be something we’re already watching…or it could be a brand-new development…a UFO (an UnForeseen Occurrence). However, the number one candidate for a catalyst in our minds is one that is already on people’s radar screens: stagflation.

We are seeing more an more signs of stagflation…with the economic data becoming a bit weaker…while the inflation numbers continue to rise. With the conti

Recent free content from Matt Maley

-

THE WEEKLY TOP 10

— 10/23/22

THE WEEKLY TOP 10

— 10/23/22

-

Morning Comment: Can the Treasury market actually give the stock market some relief soon?

— 10/21/22

-

What Do 2022 and 1987 Have in Common?

— 10/19/22

-

Morning Comment: Which is it? Is stimulus bullish or bearish for the stock market?

— 10/17/22

-

Morning Comment: Peak Inflation is Becoming a Process Instead of a Turning Point

— 10/13/22

-

{[comment.author.username]} {[comment.author.username]} — Marketfy Staff — Maven — Member

- 1 Campus Martius, Suite #200Detroit, MI 48226

- +1 877 440 9464