The NEW Daily Decision for 10.11.18 - Assuming The Worst

The State of the Markets:

Not surprisingly, I spent much of yesterday afternoon on the telephone speaking with advisors about what the heck was happening in the stock market. With the Dow just five days removed from an all-time high, the 832-point plunge clearly needed some explanation. As such, I thought I'd share the crux of my conversations with everyone this morning.

In my humble opinion, the bottom line appears to be that traders are suddenly and emphatically assuming the worst going forward. The worst in terms of the Fed, inflation, interest rates, the trade war, global economic growth, and, of course, earnings.

While I always get a chuckle out of the idea that a "new narrative" could be the root cause of a one day dive of 3% - 4% in the stock market, this was the primary explanation offered up by the media on Wednesday. You see, despite the fact that there wasn't much, if anything, in the way of new macro inputs or actual news, everybody, everywhere was singing the same bearish song yesterday.

Before I get to this new narrative, I'd first like to opine that much of Wednesday's big dance to the downside appeared to be algo-induced and thus, became exaggerated in the end. From my seat, this was a classic case of algos gone wild. Put another way, the sell algos spent the afternoon chasing their tails (i.e. making the same trades at the same time over and over again) into the close.

As Exhibit A to my argument, I submit the following. From noon mountain time until the 2:00 pm, the maximum number of consecutive green bars seen on a 1-minute chart of the S&P 500 was... wait for it... 3. Oh, and each little 2 to 3-minute blip higher (there were 6 total) was promptly greeted by another big batch of red bars. So, in reviewing the daily chart, I think the word that best describes the action is "whoosh."

Call me a cynic if you must, but I personally believe the move became a bit ridiculous and was overdone. I also think that the 500- point dive on the Dow in the final 2 hours had little to do with fundamentals or even the "new narrative." No, to me, this looked more like what I like to call "hedge fund follies," where buyers stand aside and let the algos have their way until the closing bell finally rings.

This is not to say that the market narrative isn't changing or that some adjustments to the downside are not warranted. I'm simply saying that the violence seen on Wednesday is usually reserved for a reaction to news or some external event. But, this is simply the way the game is the played in this high-speed trading world we now live in.

The New Narrative

To be sure, there have been concerns/issues in the market for some time now. You know the laundry list of worries. And heck, I've been on record urging caution on a weekly basis. As I've been saying, many of my key indicators are not in their happy places.

However, the current narrative probably needs some "esplainin." So, what follows is an executive summary of what appear to be the major concerns facing the stock market.

The way I see it, the primary assumptions the bears are promoting here include:

- The Fed will overshoot

- The Trade War will get worse and become prolonged

- #GrowthSlowing

- Rising Inflation = Multiple Contraction

- Higher Rates = Lower Valuations

The Fed

Let's start with the worry that the Fed is going to make a "policy mistake" and "overshoot" with their rate-hike campaign. This fear isn't new but had been on the back burner until Jerome Powell's most recent comments. In an interview on PBS, the Fed Chairman said that rates "are a long way from neutral" and that "we may go past neutral" for a while.

The key here is the idea that the Fed's "terminal rate" (the point where the Fed stops raising rates, which is currently seen as somewhere between 3% and 3.25%) may be changing. The problem is this is new. It took traders by surprise. And it creates uncertainty.

Folks are saying that this Fed is changing the game. That the "Fed Put" is now gone. And that Powell is more hawkish that he has led on.

Personally, I don't agree with any of the above. I simply don't believe the Fed has suddenly and without warning changed their stripes. I don't think Powell is moving toward less transparency or deviating from the plan. But this appears to be what the fear (and all the associated sell programs) is based on. Can you say, "trader tantrum?"

The Trade War

Next up is the trade war. There was virtually nothing new to report on the topic yesterday. No news. No rumors. And no tweets. But when you combine the idea of a prolonged trade war, which, according to JPMorgan analysts is likely to get worse, with an antagonistic Fed and slowing global economic growth, the "R Word" (e.g. recession) becomes the assumed end game.

#GrowthSlowing

If you are scratching your head about the idea of growth slowing down, you aren't alone. After all, isn't the U.S. economy "booming" right now? So, why on earth is everybody talking about an economic slowdown?

The answer is simple. Look at the economies of China, Europe, and the emerging markets. Read the IMF's latest outlook on global growth. 'Nuff said.

Inflation

Now let's talk about the inflation issue. In case you've been too busy to study all the economic data, it is important to recognize that inflation has finally exceeded the Fed's target of 2%.

In the beginning, this was viewed as a good thing. However, now the fear is that worker shortages, higher wages, and rising input costs (see PPG's recent guidance) will cause inflationary pressures to get out of hand. This, of course, will case the Fed to respond with more rate hikes, which will slow the economy, yada, yada.

Again, I personally have a problem with this argument. From a macro standpoint, how do we get runaway inflation when the rate of economic growth is slowing around the globe? Wouldn't the concept of "peak inflation" for the cycle make more sense here?

All About The Rates

This brings us to the issue of rising interest rates. As the argument goes, rates are going to continue to rise in the months and quarters ahead. Now that the 10-year has tested 3.25% (3.248% to be exact), 3.5% surely can't be far off, and then yields will move to 4% after that, right?

The key is that increasing rates causes debt payments to rise, which lowers profits and, in turn, puts pressure on all kinds of things like home prices/affordability. And with so much debt in the system, a continued spike in rates is going to create BIG problems (or at the very least, 838 Dow points worth of problems). So cue the fear that we're about to enter a 2008-style market again.

You Can't Have It All, Can You?

While I don't begrudge our furry friends in the bear camp their arguments, many of which do indeed have merit, I hope you recognize that you probably won't see higher inflation and higher rates in a slowing growth environment. From an economic standpoint, the two simply don't mix.

So, if you want to argue that stocks need to go lower because rates and inflation are gonna be movin' on up, or that global growth will slow next year, that's fine. But c'mon, can you really expect to have both at the same time?

To be clear, I'm not saying that yesterday's shellacking wasn't justified as an overdue correction, or that it won't continue. And I can see how slowing growth could become a problem - especially for the names that are up triple digits this year. However, I think the bears are reaching a bit here with the "new narrative" and that the extreme violence seen on Wednesday (i.e. 838 points down in a single day) doesn't make complete sense.

One thing is clear though. The bears have the ball and the bull defense doesn't seem to be able to get off the filed on 3rd down. But then again, today is another day.

Thought For The Day:

Life isn't about how to survive the storm, but how to dance in the rain -unknown

Today's Portfolio Review

Current Rating Explained

This is our rating for the day. The Current Rating tells you what action we would take if we did not currently hold the position. A "Buy" rating means we would be willing to purchase the position at current prices. A "Strong Buy" suggests this would be our first choice to buy. A "Hold" rating indicates we would not make new purchases at current levels. And a "Sell" rating indicates we will likely exit the position in the near-term.

Positions Can Change

Positions often change during the trading session. Remember that we will send a Trade Alert via SMS Text Message and/or Email BEFORE we ever make a move in the models.

Disclosure

At the time of publication, the editors hold long positions in the following securities mentioned:

SSO, QLD, XLK, XLY, XLV, AAPL, MSFT, AMZN, CNC, VFC, BA, WM, TGT

- Note that positions may change at any time.

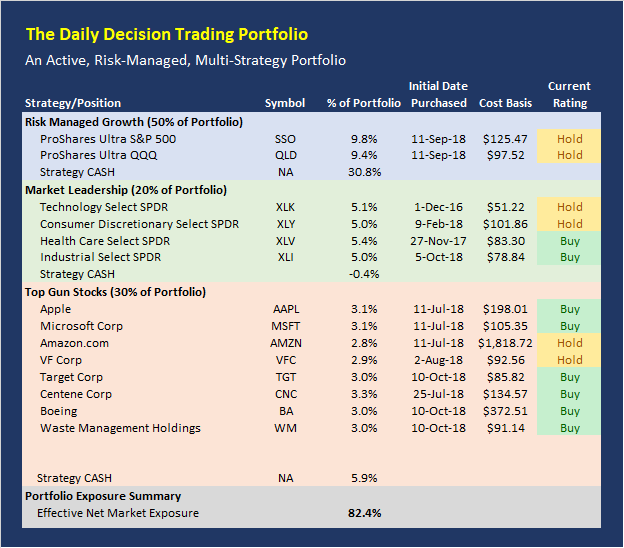

About the Portfolio:

The latest upgrade to the Daily Decision service went live on Monday, July 9. The new, state-of-the-art portfolio employs a modern, hedge fund style approach incorporating multiple methodologies, multiple strategies, and multiple time-frames. The portfolio is comprised of three parts:

- 50% Aggressive Risk-Managed Growth (up to 300% long)

- 20% Market Leaders

- 30% Top Gun Stocks

The Aggressive Risk-Managed Growth portion is made up of five trading strategies and accounts for 50% of the portfolio. The Market Leadership portion makes up 20% of the portfolio. And the Top Guns Stocks portion (10 of our favorite stocks) will make up the final 30% of the portfolio.

All three of our strategies are run in a single Marketfy model - the model is currently labeled as the LEADERS model. The goal is to make the service simpler to follow by putting everything in one place.

Wishing You All The Best in Your Investing Endeavors!

The Front Range Trading Team

NOT INVESTMENT ADVICE. The analysis and information in this report and on our website is for informational purposes only. No part of the material presented in this report or on our websites is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed nor any Portfolio constitutes a solicitation to purchase or sell securities or any investment program. The opinions and forecasts expressed are those of the editors and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations of any specific security nor specific investment advice. Investors should always consult an investment professional before making any investment.

Recent free content from FrontRange Trading Co.

-

The Lines In The Sand Are Clear

— 9/16/20

The Lines In The Sand Are Clear

— 9/16/20

-

The Question of the Day

— 8/04/20

-

Portfolio Update: 1.23.20

— 1/23/20

-

State of the Markets: Modeling 2020 Expectations (Just For Fun)

— 1/13/20

-

Current Holdings for ALL-NEW 2020 Daily Decision Model Portfolio

— 1/03/20